Darren Berg on the Run: Inside the Biggest Ponzi Scheme in Washington State History

Illustration by Michael Byers

Every night at midnight, and again at 3 and 5am, corrections officers stroll by the dormitory beds where prisoners sleep two to a cubicle and count—four, six, eight, up to more than 100—to ensure all the men are there, snoring or lying quietly before breakfast starts at 6:30.

The inmates at this camp next to the U.S. Penitentiary in Atwater, California, about 130 miles southeast of San Francisco, serve their sentences apart from some 1,200 inmates at the high-security prison. Razor wire surrounds that complex, and six guard towers form a rectangle around the perimeter. The camp, meanwhile, has minimal fencing—and security—because the prisoners are considered so low risk. There are basketball courts and a track and field and a softball diamond. The men must keep books and other belongings inside their personal lockers—only one framed photo outside is okay—and they’re generally all required to work, serving food in the cafeteria or helping maintain the site for less than a dollar a day.

Sentenced to 18 years in prison, Frederick Darren Berg had been at Atwater since 2016. He had pleaded guilty to wire fraud, money laundering, and bankruptcy fraud. Over the course of several years, Berg, now 55, cheated hundreds of investors out of more than $100 million through the Meridian Group, the company he ran in Seattle—crimes prosecutors say amounted to the biggest Ponzi scheme in Washington state history. Berg spent the money on cars, yachts, and a waterfront mansion on Mercer Island with a full-time staff. He flew between there and his homes in California on one of two private jets. He was always impeccably dressed.

At Atwater, however, Berg was issued a green uniform, just like everyone else, and he made his bed each morning with a mandatory eight-inch collar. No belongings are allowed on the windowsills, nor dust, and the floors are swept, mopped, and buffed daily. The workday for many of the camp’s prisoners starts at 7:30am, with an hour break for lunch, and ends at 3pm. A half hour later, corrections officers conduct what’s called a stand-up count and the men must wait in their cubicles as guards stride by and add them to their tally.

But on December 6, 2017, the count came up short. One of the inmates was missing.

Darren Berg was gone.

Nearly nine years earlier, investors sat around a conference table, stemmed wineglasses in front of them, and gazed up at the man standing at the head of the room as he explained why his company was different—safer, more cautious—than other investment firms.

“There’s no shortage of bad news on the doorstep,” he admitted, after tugging up the collar of a crisp white shirt. His brown hair was cut close to his head and he smiled winningly, hazel eyes crinkling behind wire frames. New York financier Bernie Madoff’s arrest a few months earlier had rattled Americans with savings entrusted to advisers like him. But Darren Berg reassured the men and women before him that day in March 2009 at Meridian’s office in downtown Seattle. “There’s no magic here,” he said. “You might think it’s magic, but it’s actually real meat and potatoes stuff.”

Berg sounded confident as he answered their questions, waving his hands in the air to emphasize a point. He had been building this company for years, he said, one loan at a time. They didn’t need to worry about their money.

Darren Berg owned several businesses, but his passion seemed to be the charter bus company MTR Western—the fulfillment of a childhood dream.

Since 2001, Berg had created and operated a series of investment funds. He told investors he would use their money to buy real estate, mortgage-backed securities, and seller-financed real estate contracts, or private mortgages—all gambles he said would generate profits to repay them with interest.

It was a risk hundreds of people were willing to take. Many of them were older and wanted to squirrel away some money for retirement. Through August 2010, from his office on the 19th floor of the Century Square building at Fourth Ave and Pike, Berg raised about $350 million from investors in about 20 states.

He often met with one of them for lunch at the now-shuttered Sixth Avenue Bar and Grill, just a half mile away. Ron Neubauer first invested with Berg in the mid-2000s, after meeting him through a close friend who had been investing with Berg for several years. As Neubauer mulled whether to sink some of his own money into Meridian’s funds, Berg showed him audited financial statements. This guy was bright—glib even—Neubauer now recalls, and he found him trustworthy. The frankness with which Berg talked about his work was heartening. Neubauer felt safe.

Berg always arrived at the restaurant—tony leather chairs, a fireplace that crackled in winter—with a check. Every month, Neubauer received a percentage of the money he had invested. The two men would order and then talk about business and, sometimes, the Mercer Island house Berg was remodeling. He had bought the mansion for nearly $5.5 million in 2007 and spent at least $5 million more renovating the 5,400-square-foot property, which had four bedrooms, four kitchens, a home theater, a pool, a deck and a dock, and a view of the Bellevue skyline gleaming on the east side of Lake Washington. The furniture, such as a king-size bed with a horse hair mattress, was custom made. A crane lifted mature trees and a stainless steel fire table into the backyard. Like his investors, Berg was profiting from the funds too.

But unnerved by the Madoff scandal, one investor, a big one, wanted to cash out. Berg couldn’t pay. By June 15, 2010, a group of investors filed a petition to force several of the funds into bankruptcy. Neubauer read about the lawsuit in the Puget Sound Business Journal and, concerned, called Berg. Berg told him not to worry. Everything’s all right, he said. You’ve got another check coming.

It arrived a few days later. Still, Neubauer was uneasy. Something seemed wrong.

Thousands of Bostonians clutching wads of money formed a line that stretched from city hall to the Niles Building, curling up the stairs and along corridors to the office of Charles Ponzi. He arrived there that morning on July 26, 1920, in a chauffeured car, biographer Donald Dunn writes in his book, Ponzi! The Boston Swindler. The Italian immigrant with a reputation for doubling investors’ money within three months raised an estimated $15 million in less than a year by convincing thousands of people to invest in an opportunity he promised would deliver big profits. All he had to do, he claimed, was buy discounted postal reply coupons and redeem them at face value. But in the schemes named for Ponzi, fraudsters pay existing investors with money collected from new investors, as opposed to investing their money and then paying them returns on that investment. The scam requires a constant flow of fresh cash to survive, and such schemes can collapse when enough investors seek their money back.

After Bernie Madoff’s fraud collapsed in 2008, wiping out billions of dollars his customers had invested, he pleaded guilty to 11 counts of fraud, money laundering, perjury, and theft. It was the largest and longest Ponzi scheme in history, and in June 2009, he received the maximum sentence for his crimes, 150 years in prison.

It was about a year later when Norman Barbosa, then an assistant U.S. attorney for the Western District of Washington, got a call about a possible significant Ponzi scheme in Seattle. The FBI and the state attorney general’s office were also getting reports from multiple sources. Darren Berg’s investors were among them.

Barbosa worked on investment fraud and white collar crime cases in the U.S. attorney’s office, but as he and other federal authorities started investigating, it quickly became clear that this one was different. The scope—the amount of money involved—was bigger than any other case in his career.

As investors succeeded in filing involuntary bankruptcies for some of Berg’s funds, though, the Mercer Island man seemed cooperative. His lawyer contacted the U.S. attorney’s office and asked for a meeting to discuss Berg’s involvement in investment fraud. Berg, said his attorney, Irwin Schwartz, wanted to come in “palms up,” and fully cooperate with any investigation.

Barbosa, FBI agent Steve Rausch, and another assistant U.S. attorney met with Schwartz on July 16, 2010. (Schwartz declined to comment for this story, saying he doesn’t discuss people he’s represented.) According to court filings by the federal government, Schwartz explained that Berg had run a series of investment funds since the early aughts but that starting around 2008, when the market began to falter, he tried to keep his funds solvent by moving money around between them, his other businesses, and personal assets. Berg thought he could keep his funds afloat until the market stabilized, Schwartz said, at which point he could sell his other companies and pay off investors.

A few days after that meeting, however, the U.S. Trustee’s Office appointed Mark Calvert, who runs investment banking firm Cascade Capital Group, to control the funds investors forced into bankruptcy. The trustee’s office interviewed multiple people for the job, Calvert recalls, choosing him for his depth and breadth of experience. Cascade Capital specializes in restructuring the finances and operations of businesses as well as bankruptcy proceedings. Calvert, who grew up in Seattle and earned a degree in finance and accounting from the University of Washington, started his career in Houston, where he worked as a CPA and a certified fraud examiner before heading to accounting firm Ernst and Young and then investment firm Alexander Hutton.

Calvert, tall, with graying hair and a pair of black cowboy boots, remembers walking over to the Century Square building on a summer day in 2010 and riding the elevator until it opened on the 19th floor. As Calvert stepped out he saw a receptionist through a glass door, which required a key to enter.

As a court-appointed trustee, investment banker Mark Calvert tried to determine what had happened at Darren Berg’s Meridian Group.

Image: Mike Kane

“I need to talk to Darren,” he said with a slight Texas drawl.

“He’s not taking anyone,” she replied through the glass. Calvert stepped to the side, out of her view, and waited for an employee to leave. He caught the door before it snapped shut again and introduced himself to the receptionist as a court-appointed trustee. She picked up the phone and called Berg, who emerged and tersely told Calvert that he was going to call security to escort him out. When Calvert told him he had a court order, they went back to Berg’s office instead.

Calvert took stock of the room, noticing on the credenza a photo of a woman and child he assumed were Berg’s wife and kid. The men spoke for almost two hours as Calvert explained what he was going to do, starting with taking over incoming mail—and mortgage payments—and then trying to determine what exactly had happened at Meridian. There were about 20 different bank accounts to parse and statements and files to review to determine if Berg had been stealing from investors, how, and for how long.

But Calvert could already see how Berg was able to raise so much money. He was a charismatic, friendly, outgoing man who tried to win over anyone he encountered—including Calvert. As Calvert and his staff took over the Meridian office suite, they met with Berg regularly and Berg appeared candid about his missteps, and keen to help Calvert navigate the many records that would allow him to piece them together.

Still, Berg refused to give up control of certain bank accounts and post office boxes, according to court filings. He provided incomplete access to banking records for his businesses, including MTR Western, a charter tour bus company. Calvert worried Berg was shielding assets from him.

Investors from another Berg fund, one that Ron Neubauer had invested in, were also wary. They presented what they knew to Randy Aliment, a Seattle attorney who specializes in commercial litigation. After reviewing the information, both lawyer and investors were sure Berg had defrauded them and that there was a good chance he’d skip town with the money he still had. Neubauer had stopped receiving checks, and he wasn’t the only one. Pressure was growing on Berg, and they worried the stakes were high enough he’d run. They sought permission from a judge to seize his assets and on July 27, 2010, accompanied by King County sheriff’s deputies, Aliment and his colleagues scattered to Berg’s Mercer Island house, Seattle office, and a downtown condo where Berg sometimes stayed. In case Berg had stashed artwork or other valuables in his yacht and planned to flee for a foreign port, Aliment had arranged for a helicopter to stand by. But as crews were dragging furniture out of Berg’s homes and business in the surprise raids, it became clear the helicopter was unnecessary. Berg showed up at his office and soon after filed for personal bankruptcy, putting the seizure on hold.

There was a third property in King County that Berg owned and that Aliment didn’t know about, though; a house in the Magnolia neighborhood. And the next day, Berg quietly sold it for nearly $400,000. Farther south, in Oregon, was yet another home that Berg had paid for. But this one he had built for his mother.

Ron Neubauer began investing with Darren Berg in the mid-2000s. To this day, he considers Berg the most convincing person he’s ever done business with.

Image: Mike Kane

FREDERICK Darren Muskopf was born in Ashland, Oregon, and grew up in Grants Pass, about an hour northwest, where he lived in a pink rambler with his mom, dad, and three siblings. He was the youngest—an obedient, outgoing, and industrious kid who patrolled the street on his Schwinn, sometimes pedaling to his neighbors’ homes to take care of their dogs or selling cherries in his grandfather’s yard.

His father, however, considered him a sissy. The family patriarch supported his wife and children as a butcher, and later as a car salesman and river guide, and, sober, he could be funny. But he drank too much, and turned mean. Though he saved his beatings for his two older sons, they took it out on the baby of the family. His mother and sister were the only ones who seemed to love the youngest Muskopf as he was.

He had few friends as a boy and when he was eight, he created an alter ego named Rod Taylor, a smart, invincible character who never failed—who was admired. He set up a desk and went into business running an imaginary bus company. His grandfather was a Greyhound bus driver, and he often talked about his work. Muskopf spent hours in his play world, away from the chaos of his real life.

He was a teenager when his parents divorced in 1975, and after his mother remarried he changed his last name from Muskopf to his stepfather’s surname, Berg. A few years later he left Grants Pass for Eugene, where he enrolled in the University of Oregon.

After pledging to the Pi Kappa Alpha fraternity, Berg was elected treasurer. Michael Stone, an alumni adviser to the fraternity at the time, later described him to CNBC as a “ball on fire.” In college, Stone said, Berg had his own charter bus company—just like Rod Taylor. Among Berg’s duties as the fraternity’s financial guardian was collecting rent from his frat brothers, but Stone eventually got a call from the landlord; where was the money?

Berg, it seemed, had taken as much as $21,000 to fund his bus company. He sounded righteous denying the accusation in a letter to Stone.

“A word for the record,” Berg wrote. “I have, at no time, ever ‘embezzled’ any funds from Pi Kappa Alpha Fraternity. What an erroneous assumption. It’s for this reason that I welcome your audit. As always, you will find a reason for everything I have done. My bookkeeping will be no exception. Any money deposited into any account will have a tangible and reasonable explanation.”

He left the fraternity, though, and dropped out of the university and made for Portland. A few years later, in the late ’80s, Berg was tangled up in criminal allegations again. He was convicted of bank fraud in the district of Oregon for stealing approximately $30,000 in a check kiting scheme, a kind of fraud that makes it look like there’s more money in a bank account than there really is so checks won’t bounce.

The judge didn’t give him any jail time; he was sentenced to probation. Berg kept heading north, to Seattle.

As federal authorities continued to investigate whether Berg had misappropriated money through his Meridian investment funds, Norman Barbosa, the U.S. assistant attorney, felt like he was working on a drug case, not a white collar crime. Fraud cases are generally slow, doddering toward a possible conviction. Berg’s unfurled fast.

Calvert was likewise startled by the sheer velocity with which money moved between Berg’s accounts. And some of the records were completely fabricated.

Many of Berg’s investments, as he pitched them to investors, involved buying private mortgages and collecting the loan payments from borrowers. Moss Adams, which was auditing Berg’s funds, wanted to confirm borrowers’ identities by mailing loan confirmation letters. Only the borrowers weren’t real. Berg opened dozens of private post office boxes in August 2007 under fake names, listed the addresses on fake loan files, and forwarded any correspondence sent to the PO boxes to an address in Seattle. Then he completed the confirmations himself and mailed them back to the auditor.

Calvert’s forensic accounting of Berg’s business turned up other anomalies. More than $32 million of investors’ money was spent on MTR Western, the bus company. More than $11 million went to Meridian Greenfield, a construction company Berg owned, and his Mercer Island home. Over $5 million was spent on Lear jets, and approximately $3 million funded yachts.

As the summer of 2010 sped along, more of Berg’s funds were added to bankruptcy proceedings and a bankruptcy attorney was tapped to be the trustee for Berg’s personal estate, including MTR Western, subsidiary bus companies, and his homes.

Before his arrest Darren Berg enjoyed yachts and a $5.5 million Mercer Island mansion.

Image: Courtesy CC Bain and Cascade Capital Group

On October 13, 2010, a consultant working for the trustee discovered a new bank account in Berg’s name, according to court records. He had opened it more than a month prior but, during a four-hour briefing with law enforcement on September 20, Berg didn’t mention it when asked to list all the bank accounts he continued to control.

The consultant noticed $145,000 had been transferred to the account days after Berg opened it from another account in the name of DB517 LLC. Berg had opened that account in February and not long after, $225,000 was wired to it.

Berg explained that the money came from consulting work he started in early August 2010, after he declared personal bankruptcy. The court order in those proceedings entitled him to keep any money earned after the Chapter 11 filing.

Contracts for the consulting jobs showed the work was related to owning corporate jets. Investigators could only find one of the people who supposedly signed the agreements enlisting Berg for work. His name was spelled wrong and, the alleged consultee said, the signature was fake. The money was actually from the sale of the Magnolia house that initially escaped investigators’ notice, according to prosecutors, and Berg spent it on lease payments for two Porsches, 12 months advance rent on an apartment in Los Angeles, an Audi convertible, insurance on jet skis and a yacht—and a retainer for a criminal defense attorney.

Prosecutors charged Berg with nine counts of wire fraud and one count of money laundering. On October 21, 2010, he was arrested. The government asked the judge to detain him before trial. They worried he was a flight risk. Authorities had discovered evidence that Berg had tried to establish an offshore trust in Belize. He said he had been exploring ways to protect the assets in his bus company—to insure them—but prosecutors pointed to the move as proof Berg was trying to run.

Berg had claimed he wanted to give the government a full accounting of his investment fund activity, to cooperate. But, a detention motion states, “Since that time, Mr. Berg’s cooperation has been inconsistent and manipulative.”

The judge ordered Berg to stay behind bars, and the defendant pleaded not guilty to all allegations. On November 18, a new indictment came down with additional charges: another count of money laundering and one count of bankruptcy fraud.

Berg insisted that his business had been legitimate, but that by 2008, he was in “survival mode.” The crumbling economy led him to act out of desperation to salvage Meridian and keep investors satisfied, he said.

Barbosa had heard that argument before. Often, he says, fraudsters will focus on their activity that wasn’t illegal, as if that honesty will tip the scales again in their favor.

“You can’t tell lies in order to get people to part with their money,” he says. “And throughout the whole scheme, Berg was lying aggressively about the nature of investments, quality of investments, and strength of the funds.”

The two sides reached a plea agreement nearly a year later. On August 2, 2011, Berg pleaded guilty to one count of wire fraud, one count of money laundering, and one count of bankruptcy fraud. He was sentenced to 18 years in federal prison the following year.

Ron Neubauer was surprised when he realized Berg had probably defrauded him, and then he felt angry. More than five decades ago, Neubauer was an assistant U.S. attorney prosecuting people accused of running Ponzi schemes. But Berg never roused his suspicions. Even today, among all the people he’s made investments with, Berg was the most convincing and seemed the most trustworthy. Then again, Neubauer says, “I never met a sociopath I didn’t like.”

He was in Kane Hall at the University of Washington on August 30, 2010, when Calvert assembled more than 500 investors for a meeting and revealed to many for the first time that he thought they had invested in a Ponzi scheme. Berg’s business didn’t start out as a Ponzi, Calvert explained, and there were even some funds that appeared lawful. But, he said, Berg had been making unauthorized loans from the funds they had invested in to pay for interest payments, MTR Western and the subsidiary bus companies, lavish parties for his employees, and more.

Some investors cried sitting in the auditorium that morning. Calvert estimated that, on average, they could recover between 9 and 20 percent of the original amount of money they handed over to Berg. As of March, that’s looking more like 26 to 28 percent. Calvert continues to liquidate assets. Still, some investors had to go back to work. Others have died. Berg’s Ponzi lasted longer than most because about half of the cash invested was retirement money. His clients were older. They were also successful, intelligent business people and professionals. And yet, Berg duped them.

Sitting in a coffee shop in Bellevue in January 2018, Craig Edwards, dressed in a red plaid shirt and slacks, recalls how Berg said he was a law school graduate and how that legal background helped him in the real estate business. Edwards had friends who invested with Berg; people and companies he trusted associated with him. One of the country’s largest accounting firms was auditing the company. Edwards invested $50,000 as a trial. He wanted the money in a conservative fund. Soon, he was receiving monthly checks for about $300, or 7 percent of that principal amount annually.

In a letter to a U.S. District judge, sent before Berg was sentenced, Berg’s mother wondered what responsibility her son’s investors bear in all this—and how they couldn’t suspect something was amiss. “They too must be culpable for a small percentage of the guilt, as savvy investors, for letting their greed overtake their reason,” she said.

A former employee who worked for Berg for four years, however, says his former boss kept people in silos. Everyone had to communicate through him. And, suspects the employee—who asked to remain anonymous for fear of reprisal—Berg tailored his persona to each individual, sizing them up and deciding how he needed to act to get what he wanted.

His image was important to him, the employee said. In 2008, he rented out the then EMP Sky Church during a Professional Convention Management Association event to woo business for his bus company, paying Ben Folds and John Mayer to perform at the intimate gathering. (Mayer seemed to later wink at the moment in the movie Get Hard, in which he performs at the birthday party of Will Ferrell’s fraudster character, who is arrested midset.)

Berg also fussed over the appearance of his buses, those once imaginary vehicles under the care of Rod Taylor that were now real, ferrying professional sports teams like the Seattle Seahawks. He took pride in those buses, refusing to let them travel on gravel or in snow. They had oak floors, and the drivers, among about 300 employees Berg had hired, were dressed in fine Nordstrom uniforms. But in the downtown Seattle office, his behavior was not always so polished.

He threw office supplies, like staplers, and his cell phone when he was upset, busting them so badly they needed to be replaced. He kept the staff off balance and he often seemed stressed, and angry. After such outbursts he would never admit he was wrong, the anonymous employee said. “He would just defend.”

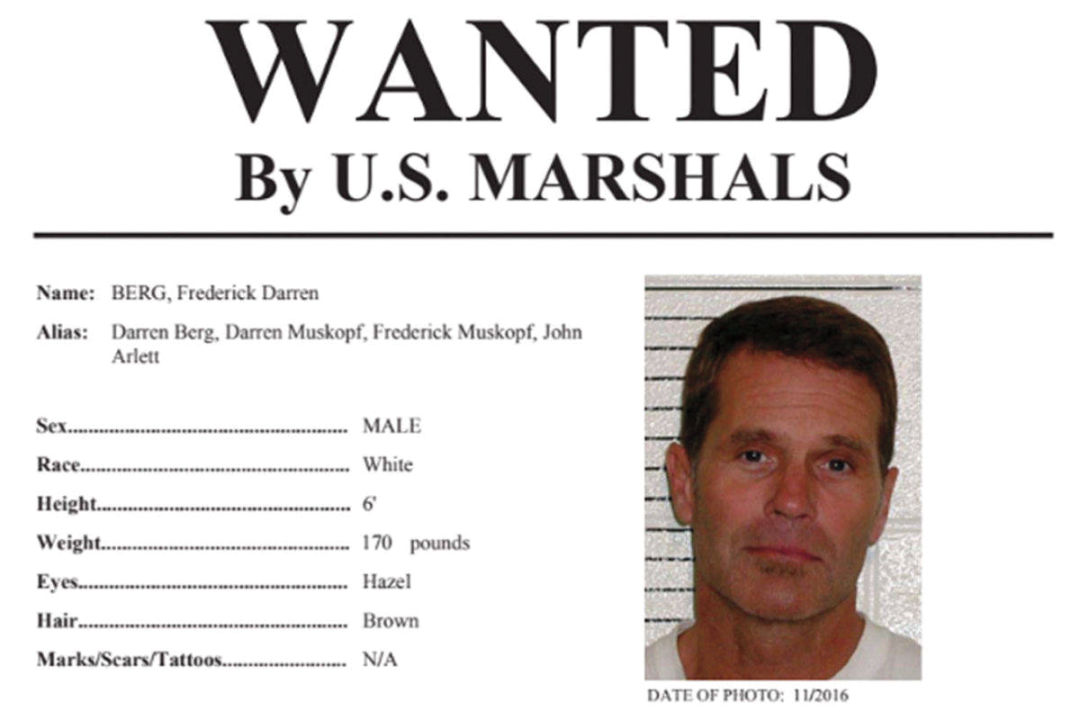

As of publication, Darren Berg is on the run from U.S. Marshals after escaping a California federal prison in December 2017.

On December 7, 2017, the U.S. Marshals Service issued a wanted poster for Frederick Darren Berg. The Federal Bureau of Prisons had alerted the agency about Berg’s escape, and the deputies tasked with tracking down the country’s fugitives asked residents in California, Oregon, and Washington with any information about his whereabouts to contact them. As of press time, Berg is still missing.

He was working on the grounds when he walked away, bringing the number of prisoners to escape from the facility since 2011 to eight, according to the bureau. The agency declined to answer questions about Berg, who transferred to Atwater from a low-security facility in Lompoc, California, where he served the first part of his sentence. The U.S. Marshals deputy leading the investigation into Berg’s disappearance had little to add about Berg’s possible location.

Some investors have wondered if, eight years later, he finally made it to Belize, or somewhere else abroad. It’s possible he liquidated assets that escaped the attention of the bankruptcy trustees and authorities.

“He is an incredibly intelligent person,” Barbosa says. “I have no doubt that he thought long and hard about this and had a plan that he executed over a number of years.”

News of Berg’s escape rankled his investors. They had wanted a tougher prison sentence. Many of them had to delay retiring, take additional jobs, and sell their homes. Prosecutors expected that some of them would be forced into their own bankruptcies because of Berg. At Berg’s sentencing hearing in February 2012, Richard Jones, the judge, described a “reckless disregard for his victims.” One investor puts his feelings more bluntly: “I hope he’s hiding out, wracked with paranoia in some rat-infested mosquito-ridden dung hole fearing for his shitty life!”

But Calvert expects Berg’s escape was extremely well orchestrated, and he doesn’t think Berg’s whereabouts will be discovered unless Berg wants them to be known. Others aren’t convinced that he won’t make a mistake and accidentally reveal himself.

In some ways, the speculation is an extension of the uncertainty that surrounded Berg when he was under investigation, when prosecutors wondered if he was really cooperating or just pretending. Maybe everything he disclosed to authorities, lawyers, and trustees was intentional, carefully laid tracks leading them where he wanted. Or maybe he just got caught and divulged more about his crimes than he realized.

Berg did do something wrong, his mother said recently, though she didn’t want to say much else when I called her one evening this winter.

“My experience has been no matter what’s said, the news twists it around to be what they want to make it more sensational,” she said. “No comment.”

She later sent me a book Berg wrote in prison titled My Apologies, a more than 300-page work in progress. The book, dedicated to his mother and sister, opens with a quote from Oscar Wilde’s The Importance of Being Earnest: “The truth is rarely pure and never simple.”

While Berg had fraught relationships with some employees and family members, he seemed to cherish his mother and sister. He doted on his sister’s children, she wrote in a letter to the judge before Berg was sentenced. And they worshipped him.

She recalled a moment in their childhood when Berg was three, chairs flying as their father raged, sirens blaring in the distance, and her brother oblivious, curled in bed asleep.

“I know now that this was the beginning of his mind shutting down,” she said. “The world we inhabited was too scary for him to navigate, so he went somewhere he could be safe.” He invented Rod Taylor, she says, and he never really let him go.

True Detective

The True Tale of Seattle's Sherlock Holmes

Death By Air

Why Have We Had So Many Serial Killers Here?

Feature

A Midsummer Nightmare

Year in Review