Friday Likes and Dislikes: Undoing Payday Loan Regulations

Caffeinated News

Friday LIKES & DISLIKES

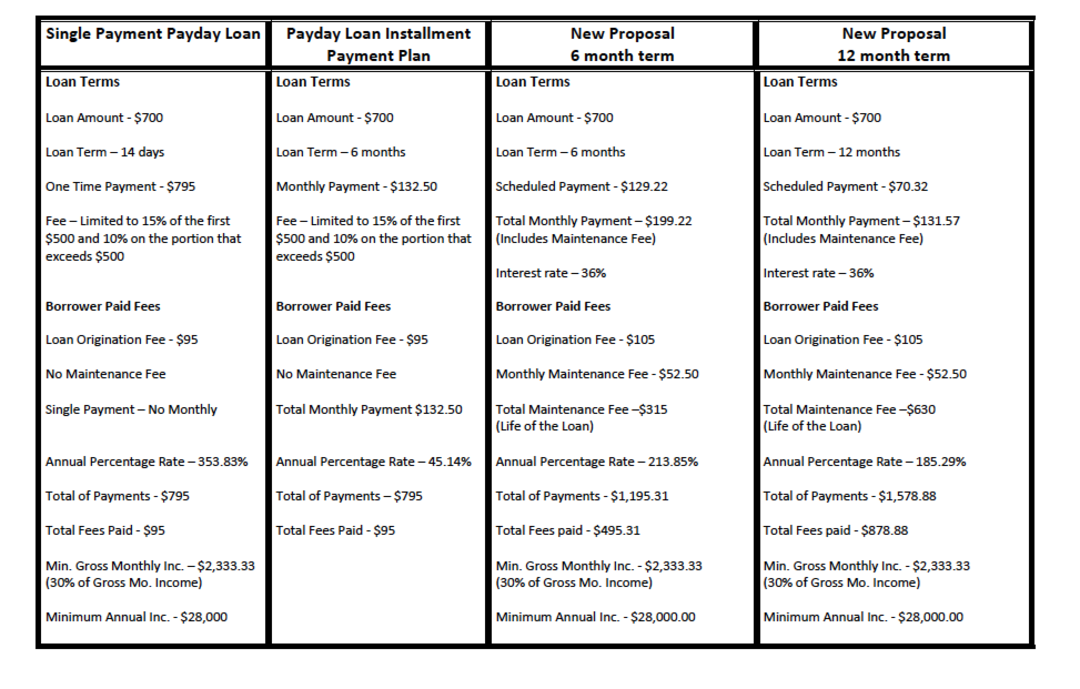

1. I DON'T LIKE that despite the success of legislation passed in 2009 regulating payday loans, both the Republican state senate and Democratic state house have passed bills out of committee this month that would undo the current rules (which cap loans at $700, cap interest at no more than 15 percent on the first $500 and no more than 10 percent on the rest, and provide a "circuit breaker" to stop borrowers from getting into a cycle of debt) by replacing payday loans with something called "Installment Loans."

Proponents of the bill, including Seattle Democrats such as representatives Eric Pettigrew, Sharon Tomiko Santos, and Gael Tarleton, argue that the longer minimum term of installment loans (six months to a year versus a borrower's next payday to 45 days) gives the consumer more flexibility to repay.

But opponents, such as representative Cindy Ryu (the lone no vote in the house government operations committee), point out that the new loans create higher interest payments—a 213.849 percent APR versus the current 45.14 percent APR. For example: A $700 loan at the six-month term would cost $1,195.31. For a current payday loan for two weeks (or up to 45 days) it would cost the consumer $795.

Here's a compare and contrast chart from Washington State Department of Financial Institutions.

There doesn't seem to be a reason to undo the 2009 rules. Check out more results from the Washington State Department of Financial Institutions: The average payday loan amount is $380.17. (The new rules would allow a $1,000 loan.) The annual average cost to borrowers to use a loan is $205, one of the lowest in the country. The median number of loans is three, among the fewest in the country. The APR is the third lowest in the country. And the average loan length is one of the longest at four weeks.

And defaults have declined dramatically:

2. I DON'T LIKE that a new poll found that more people in the Puget Sound region are against raising the gas tax to pay for transportation than are for it: 48 percent versus 30 percent.

3. However, I LIKE the numbers because (maybe?) they indicate that voters are realizing the gas tax is an outmoded and regressive way to cover transportation costs.

For example, the poll also found that governor Jay Inslee's idea—charging the oil companies themselves—might be a better approach.

Word is the state senate may vote on the transportation package today, which includes an 11.7 cent gas tax and no sign of Governor Inslee's proposal for a $12 chit per carbon ton per year on the state's biggest polluters, putting $400 million of the money toward transportation spending.

4. And neither a LIKE nor a DISLIKE, but I'd LIKE to point out a follow up to yesterday's data download on downtown Seattle. (The Downtown Seattle Association released a big report yesterday, morning.)

In an effort to dispel the notion that downtown Seattle, as opposed to the rest of the city, is more exclusive, I added some stats to the DSA's report, noting that 36 percent of the subsidized housing tracked by the Office of Housing is in downtown Seattle.

Here's some more context: That number represents about 25 percent of all the housing stock in downtown Seattle. Seven percent of the housing stock outside downtown is subsidized. So, proportionally, downtown has more than three times as much subsidized housing.

5. Finally, crime stats were strangely absent from the DSA stats.

The City of Seattle says that in downtown, major crime has increased over 35 percent since 2011.